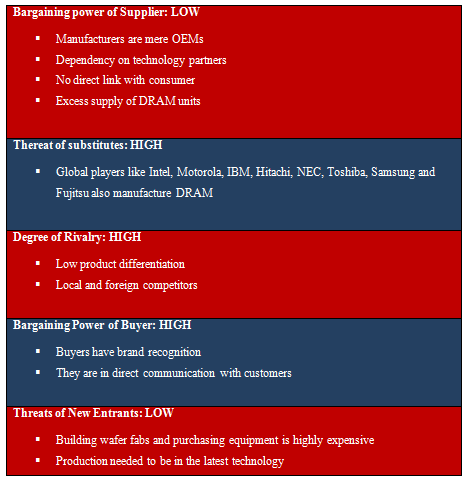

Bargaining Power of Supplier:

The vendor in the Taiwanese Accounting For Manufacturing Companies market has a reduced negotiating power although that the sector has supremacy of 3 players including Powerchip, Nanya and ProMOS. Accounting For Manufacturing Companies suppliers are mere original equipment manufacturers in critical partnerships with foreign players in exchange for innovation. The 2nd factor for a low bargaining power is the fact that there is excess supply of Accounting For Manufacturing Companies devices because of the large range production of these dominant industry players which has actually reduced the cost per unit and boosted the negotiating power of the customer.

Threat of Substitutes & Degree of Rivalry:

The risk of substitutes out there is high offered the fact that Taiwanese makers compete with market show to worldwide players like Intel, Motorola, IBM, Hitachi, NEC, Toshiba, Samsung and also Fujitsu. This indicates that the market has a high level of rivalry where suppliers that have style and advancement capabilities in addition to manufacturing knowledge may be able to have a greater bargaining power over the marketplace.

Bargaining Power of Buyer:

The market is dominated by players like Micron, Elpida, Samsung and also Hynix which even more decrease the buying powers of Taiwanese OEMs. The fact that these critical players do not permit the Taiwanese OEMs to have accessibility to modern technology shows that they have a higher negotiating power relatively.

Threat of Entry:

Dangers of entry in the Accounting For Manufacturing Companies production sector are low because of the truth that building wafer fabs and also purchasing equipment is extremely expensive.For just 30,000 devices a month the resources demands can vary from $ 500 million to $2.5 billion depending upon the dimension of the systems. The production needed to be in the most current innovation as well as there for new players would not be able to contend with leading Accounting For Manufacturing Companies OEMs (initial tools suppliers) in Taiwan which were able to take pleasure in economic climates of scale. In addition to this the existing market had a demand-supply imbalance and so oversupply was already making it challenging to permit new gamers to take pleasure in high margins.

Firm Strategy:

Because Accounting For Manufacturing Companies manufacturing uses conventional processes and conventional and specialized Accounting For Manufacturing Companies are the only 2 classifications of Accounting For Manufacturing Companies being produced, the processes can conveniently make use of mass production. While this has actually led to schedule of innovation as well as range, there has been disequilibrium in the Accounting For Manufacturing Companies market.

Threats & Opportunities in the External Environment

As per the inner as well as external audits, opportunities such as strategicalliances with innovation partners or development with merger/ acquisition can be explored by TMC. An action towards mobile memory is likewise a possibility for TMC particularly as this is a particular niche market. Risks can be seen in the type of over reliance on foreign gamers for innovation as well as competition from the US as well as Japanese Accounting For Manufacturing Companies manufacturers.

Porter’s Five Forces Analysis