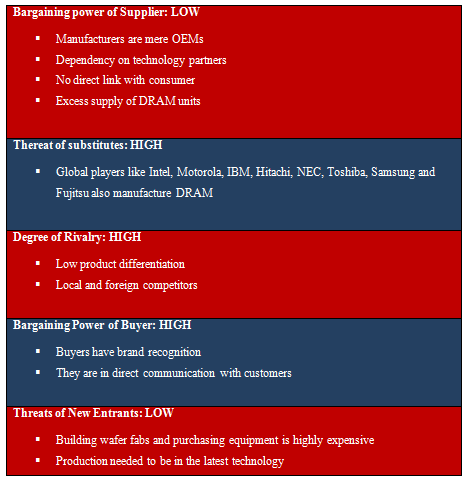

Bargaining Power of Supplier:

The distributor in the Taiwanese Deferred Tax Assets In Basel Iii Lessons From Japan market has a reduced bargaining power despite the fact that the sector has dominance of three players including Powerchip, Nanya and also ProMOS. Deferred Tax Assets In Basel Iii Lessons From Japan manufacturers are mere initial tools manufacturers in tactical partnerships with international players for modern technology. The 2nd reason for a reduced bargaining power is the fact that there is excess supply of Deferred Tax Assets In Basel Iii Lessons From Japan devices due to the huge scale production of these dominant market gamers which has decreased the cost each and also increased the bargaining power of the purchaser.

Threat of Substitutes & Degree of Rivalry:

The hazard of substitutes in the market is high offered the reality that Taiwanese makers compete with market share with international players like Intel, Motorola, IBM, Hitachi, NEC, Toshiba, Samsung and also Fujitsu. This indicates that the marketplace has a high level of rivalry where makers that have design and growth capabilities in addition to producing proficiency may be able to have a greater bargaining power over the marketplace.

Bargaining Power of Buyer:

The marketplace is controlled by players like Micron, Elpida, Samsung and also Hynix which further decrease the buying powers of Taiwanese OEMs. The truth that these tactical players do not enable the Taiwanese OEMs to have access to technology suggests that they have a higher bargaining power fairly.

Threat of Entry:

Hazards of entry in the Deferred Tax Assets In Basel Iii Lessons From Japan production market are reduced due to the truth that structure wafer fabs and also acquiring equipment is very expensive.For simply 30,000 units a month the resources requirements can vary from $ 500 million to $2.5 billion depending on the size of the systems. In addition to this, the manufacturing needed to be in the most up to date innovation and also there for new gamers would certainly not have the ability to take on dominant Deferred Tax Assets In Basel Iii Lessons From Japan OEMs (original tools makers) in Taiwan which were able to take pleasure in economic climates of scale. In addition to this the current market had a demand-supply discrepancy therefore surplus was currently making it difficult to permit brand-new gamers to delight in high margins.

Firm Strategy:

Given that Deferred Tax Assets In Basel Iii Lessons From Japan manufacturing makes use of typical procedures and basic and specialty Deferred Tax Assets In Basel Iii Lessons From Japan are the only two groups of Deferred Tax Assets In Basel Iii Lessons From Japan being manufactured, the procedures can conveniently make use of mass production. While this has led to accessibility of modern technology as well as range, there has actually been disequilibrium in the Deferred Tax Assets In Basel Iii Lessons From Japan sector.

Threats & Opportunities in the External Environment

According to the internal and outside audits, opportunities such as strategicalliances with modern technology companions or development through merging/ procurement can be explored by TMC. An action towards mobile memory is additionally an opportunity for TMC specifically as this is a particular niche market. Risks can be seen in the kind of over dependence on international players for technology as well as competitors from the United States and Japanese Deferred Tax Assets In Basel Iii Lessons From Japan producers.

Porter’s Five Forces Analysis