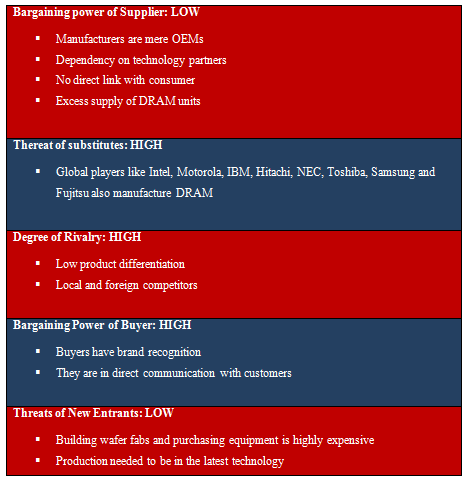

Bargaining Power of Supplier:

The supplier in the Taiwanese Introduction To Responsibility Accounting Systems sector has a low bargaining power despite the fact that the market has supremacy of 3 players including Powerchip, Nanya and also ProMOS. Introduction To Responsibility Accounting Systems manufacturers are plain original devices producers in strategic alliances with international gamers in exchange for innovation. The 2nd factor for a low bargaining power is the fact that there is excess supply of Introduction To Responsibility Accounting Systems systems as a result of the large scale production of these leading industry players which has actually lowered the price per unit and enhanced the negotiating power of the buyer.

Threat of Substitutes & Degree of Rivalry:

The threat of alternatives out there is high provided the fact that Taiwanese suppliers take on market share with international gamers like Intel, Motorola, IBM, Hitachi, NEC, Toshiba, Samsung as well as Fujitsu. This suggests that the marketplace has a high degree of rivalry where makers that have design as well as growth capabilities in addition to producing knowledge may be able to have a higher bargaining power over the marketplace.

Bargaining Power of Buyer:

The marketplace is controlled by gamers like Micron, Elpida, Samsung and Hynix which even more minimize the purchasing power of Taiwanese OEMs. The fact that these tactical gamers do not allow the Taiwanese OEMs to have accessibility to modern technology suggests that they have a greater negotiating power relatively.

Threat of Entry:

Risks of entrance in the Introduction To Responsibility Accounting Systems production market are reduced due to the fact that structure wafer fabs and also acquiring equipment is highly expensive.For just 30,000 systems a month the funding requirements can vary from $ 500 million to $2.5 billion depending upon the size of the devices. Along with this, the production required to be in the current modern technology and there for brand-new players would certainly not have the ability to take on dominant Introduction To Responsibility Accounting Systems OEMs (original tools suppliers) in Taiwan which were able to appreciate economic climates of range. The present market had a demand-supply inequality and also so oversupply was currently making it hard to permit brand-new players to appreciate high margins.

Firm Strategy:

The area's production firms have actually relied on a method of mass production in order to decrease prices with economic situations of scale. Since Introduction To Responsibility Accounting Systems manufacturing utilizes basic processes and standard and specialized Introduction To Responsibility Accounting Systems are the only 2 categories of Introduction To Responsibility Accounting Systems being made, the processes can easily make use of automation. The sector has dominant manufacturers that have formed alliances for modern technology from Oriental and also Japanese companies. While this has actually caused accessibility of innovation and also scale, there has actually been disequilibrium in the Introduction To Responsibility Accounting Systems market.

Threats & Opportunities in the External Setting

As per the internal as well as outside audits, possibilities such as strategicalliances with modern technology companions or growth via merger/ procurement can be explored by TMC. In addition to this, a relocation towards mobile memory is also an opportunity for TMC especially as this is a specific niche market. Risks can be seen in the type of over reliance on international gamers for innovation as well as competition from the United States as well as Japanese Introduction To Responsibility Accounting Systems manufacturers.

Porter’s Five Forces Analysis